Is bitcoin’s four-year cycle broken?

Key points

- Bitcoin’s price has historically followed a four-year cycle aligned with halving events.

- The recent bitcoin all-time high in October 2025 has market participants questioning whether the current cycle is over.

- Institutional capital and a reduced supply shock at each halving are changing the dynamics of bitcoin’s price.

- Supporters of the four-year cycle say the same timeline is repeating.

- Proponents of a longer bitcoin cycle cite global liquidity and demographic changes as key reasons why the cryptocurrency’s gains will extend beyond a four-year timeframe.

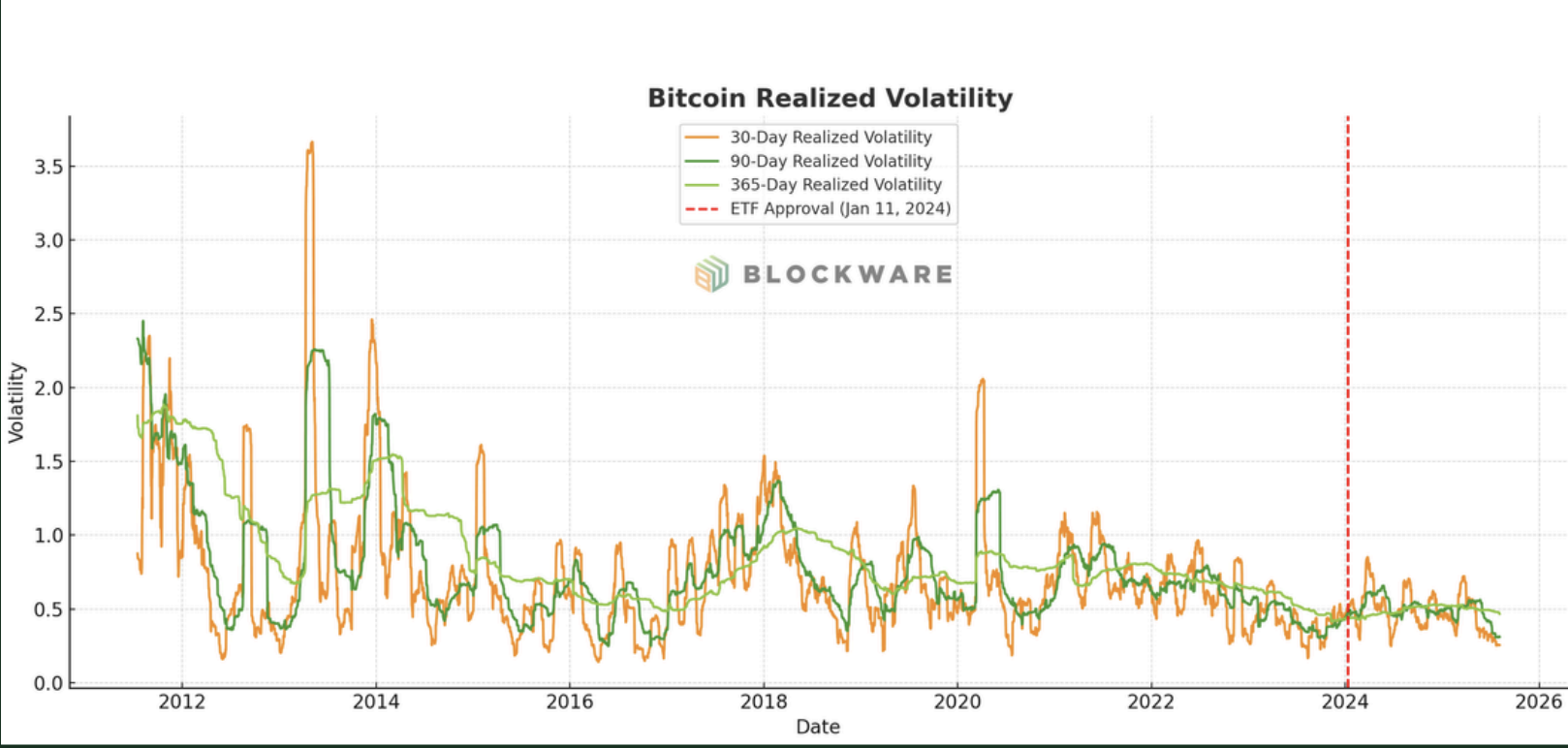

Since bitcoin’s inception in 2008, its price has followed a predictable four-year cycle, largely driven by retail activity. Every four years, following bitcoin's halving event, which cuts new supply by 50%, a steep bull run typically occurs. This bull run is followed by a sharp correction of up to 80% in the 12 months following the market cycle top. Unlike previous cycles, institutional money and macro correlation lowered bitcoin’s volatility since the last cycle low in November 2022.

The changes to the cryptocurrency ecosystem beg the question: Is bitcoin’s four-year cycle broken? There are compelling cases for either side of the argument, and we explore these below. Keep reading to learn more.

What were the gains in previous bitcoin cycles?

Bitcoin’s previous four-year cycles have seen the cryptocurrency make strong gains then steep losses. The gains and losses were:

- 2012: cycle low of US$12 rallied to US$1,150, before dropping 85%

- 2016: US$650 to US$20,000, and then crashed 80%

- 2020: from US$8,700 to US$69,000, and then a 75% correction

- 2022: cycle low of US$15,460 to US$126,198 (+716%). Price down 46% from October 6, 2025 all-time high (ATH) as at March 2026.

The current cycle saw bitcoin rally to a new all-time high (ATH) of US$126,198 on October 6, 2025. The last halving was on April 20, 2024. Since this most-recent halving to December 2025, bitcoin rallied 100% to the October 6 ATH — a much smaller post-havling rally than previous cycles as increased adoption and institutional capital lowered bitcoin’s volatility.

What has changed bitcoin’s four-year cycle?

Three months before the April 2024 halving, bitcoin spot exchange-traded funds (ETFs) started trading on January 11. The entrance of institutional capital into the market has potentially caused steadier price movements, both to the upside and downside, compared to previous cycles that were characterised by a blow-off top. While this “blow-off top” scenario may still occur this cycle, proponents of bitcoin’s four-year cycle breaking indicate that the asset may no longer experience significant swings anymore, particularly to the upside.

Another key difference this cycle, compared to previous cycles, is that a new all-time high was reached before the April 2024 halving as institutional demand potentially tempers the large swings typical of retail trading in earlier cycles.

Before institutional capital entered crypto, the previous bitcoin cycles followed a similar timetable. The time from the cycle low to the cycle high was typically around 1,060 days, while the time from the cycle high to the next low was around 370 days. The timing between bitcoin’s previous cycle lows and highs is outlined below.

| Cycle dates | Market | Count (days) |

|---|---|---|

| Cycle low Jan 14, 2015 → ATH Dec 17, 2017 | Bull | 1,068 |

| ATH Dec 17, 2017 → Cycle Low Dec 15, 2018 | Bear | 363 |

| Cycle Low Dec 15, 2018 → ATH Nov 10, 2021 | Bull | 1,061 |

| ATH Nov 10, 2021 → Cycle Low Nov 21, 2022 | Bear | 376 |

| Cycle Low Nov 21, 2022 → most-recent ATH Oct 6, 2025 | Bull | 1,050 (assuming bull run over) |

| Potential bear | ||

| 149 days (-46%) |

Source: CoinMarketCap

Assuming the time from the October 6, 2025 ATH to the recent declines was the beginning of a bear market, there could be approximately 220 further days (to mid-October 2026) of potential downside before bitcoin’s price bottoms.

Importantly, this scenario relies only on the average length of each bull and bear market, and there are several other factors influencing bitcoin’s price. These factors are detailed in the following sections.

Institutional capital is making bitcoin less volatile

Before bitcoin ETFs launched, the cryptocurrency’s annualised realised volatility typically exceeded 150%. Since January 2024, bitcoin’s volatility has compressed, with spikes preceding profit-taking less violent, and drawdowns milder than previous cycles. Further, on-chain data demonstrates that in the post-ETF era, market participants take profit at lower multiples than previous cycles. Currently, the net unrealised profit/loss multiple has ranged between 45% and 65%, meaning the dips are bought quickly, while pumps are sold just as quickly, too.

Since the crypto sell-off that was exacerbated by the record liquidation event on October 10, when US$19 billion in leveraged positions were liquidated, bitcoin’s net unrealised profit/loss (NUPL) declined to 19% as of late-February 2026. A high NUPL over 50% indicates that the market is in a greed-driven peak, while a low NUPL indicates fear or capitulation. The declining NUPL from the October all-time high supports the thesis that the four-year cycle is still intact.

Global macro has become more influential on bitcoin’s price

Previous bitcoin halvings saw supply drastically reduce, which caused a larger degree of scarcity than the most-recent halving. In the 2024 halving, bitcoin’s supply reduced to 0.85% from 1.7%. Further, almost 94% of all bitcoin has been mined, meaning that the supply shock becomes more subdued with each halving.

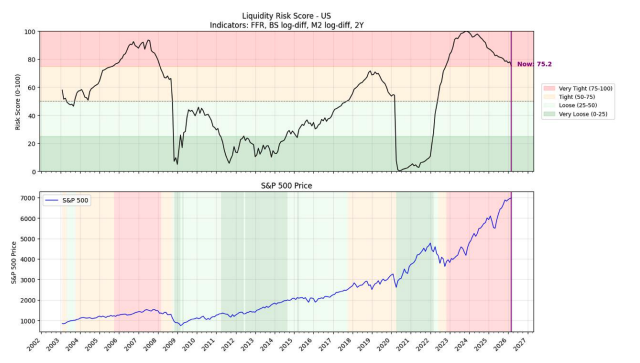

Like other risk assets, bitcoin has become correlated with the global M2 money supply. Throughout 2022, when central banks were raising interest rates to curb inflation, bitcoin declined along with other risk assets. And as global liquidity began to grow again from 2023 to 2025, bitcoin’s price appreciated.

Market participants will presumably be closely watching the U.S. Federal Reserve's monetary policy agenda throughout the remainder of 2026, especially as quantitative tightening ended in December 2025. While liquidity won’t immediately spike, monitoring how risk assets and bitcoin respond to the adjustment in monetary policy will provide an indication of whether bitcoin continues selling off to a low in late 2026, which would align with the four-year cycle remaining intact.

Does the current global macro environment mean bitcoin’s four-year cycle is intact?

Historically, the year that follows bitcoin’s post-halving peak is characterised by compression, lower volatility expansion and declining year-to-date returns. Further, in mid-term election years, like 2014, 2018 and 2022, and late-cycle environments, bitcoin has led weakness in risk assets. It wasn’t until TradFi markets exhibited further weakness that liquidity conditions meaningfully changed, aligning with the view that risk assets like bitcoin and crypto could see upward momentum in the long term, but the right monetary policy conditions have to prevail. And those conditions require policymakers to be satisfied that substantive measures must be taken, meaning a sustained sell off across TradFi risk assets driven by persistent economic weakness. If bitcoin and other risk assets continue to decline throughout 2026 until central banks implement quantitative easing and other measures to boost liquidity, then it would be clear that bitcoin’s four-year cycle is not broken.

It’s also important to note that bitcoin’s October 2025 all-time high wasn’t accompanied by euphoria and a broader altseason. This means the downside following the peak may also be subdued. Market participants could expect slower declines, reduced speculation and longer periods of consolidation before the trend materially changes. And with the return on investment declining with each market cycle, plus Wall Street’s involvement in offering exposure to bitcoin, future rallies could be more subdued, too. Though, when compared to TradFi’s year-on-year performance, bitcoin’s previous market cycles still far outperform the major U.S. indexes.

Given there hasn’t been a clear catalyst for central banks to resume further interest rate cuts or quantitative easing, precious metals have maintained their relative strength and treasury yields have declined, the current picture in bitcoin and across crypto could indicate a late-cycle environment, where a bottom will be formed in the coming months and price (and sentiment) will turnaround when liquidity conditions ease. The charts below indicate that, while quantitative tightening ended in the U.S. in December 2025, monetary policy remains relatively restricted.

As the catalysts align to warrant lower interest rates and increased liquidity, risk assets, including crypto, may eventually attract the sustained capital flows required to see upward momentum.

What does a five-year cycle mean for bitcoin?

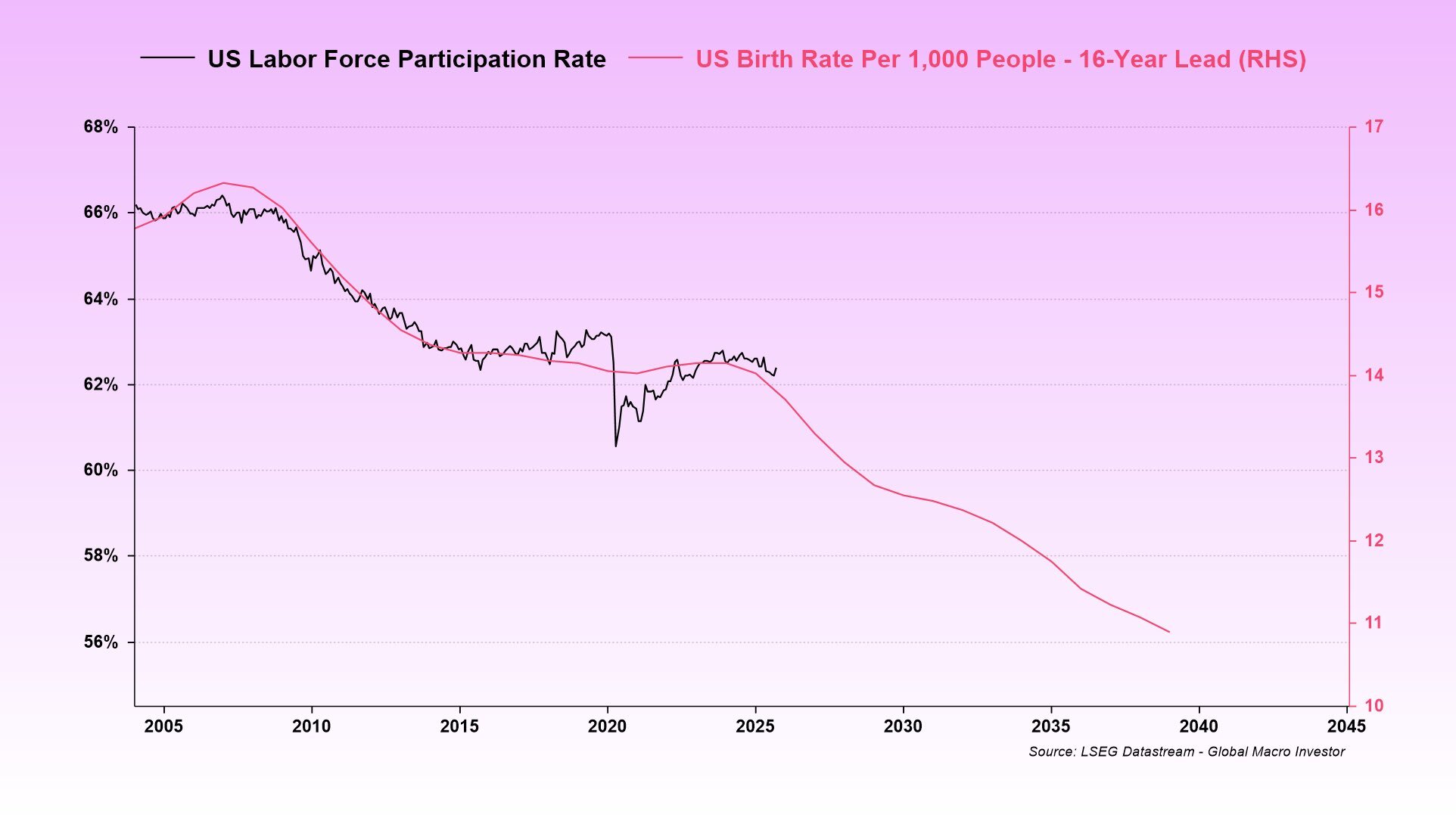

Proponents of bitcoin’s cycle extending beyond the four-year timetable cite macroeconomic factors, such as M2 money supply, demographic changes, and currency debasement, as the core reasons why bitcoin’s price movements more closely align with liquidity and business cycles. The central thesis of bitcoin’s cycle lining up with the business cycle is that, in the U.S., for example, the targeted growth rate of about 2% is used in its entirety to service debt repayments, which doesn’t fuel new growth. With the birth rate declining, population growth isn’t occurring fast enough to expand the labour force, and, in turn, fuel further economic expansion. In this sort of scenario, the central bank must stimulate growth through monetary policy measures such as quantitative easing (QE).

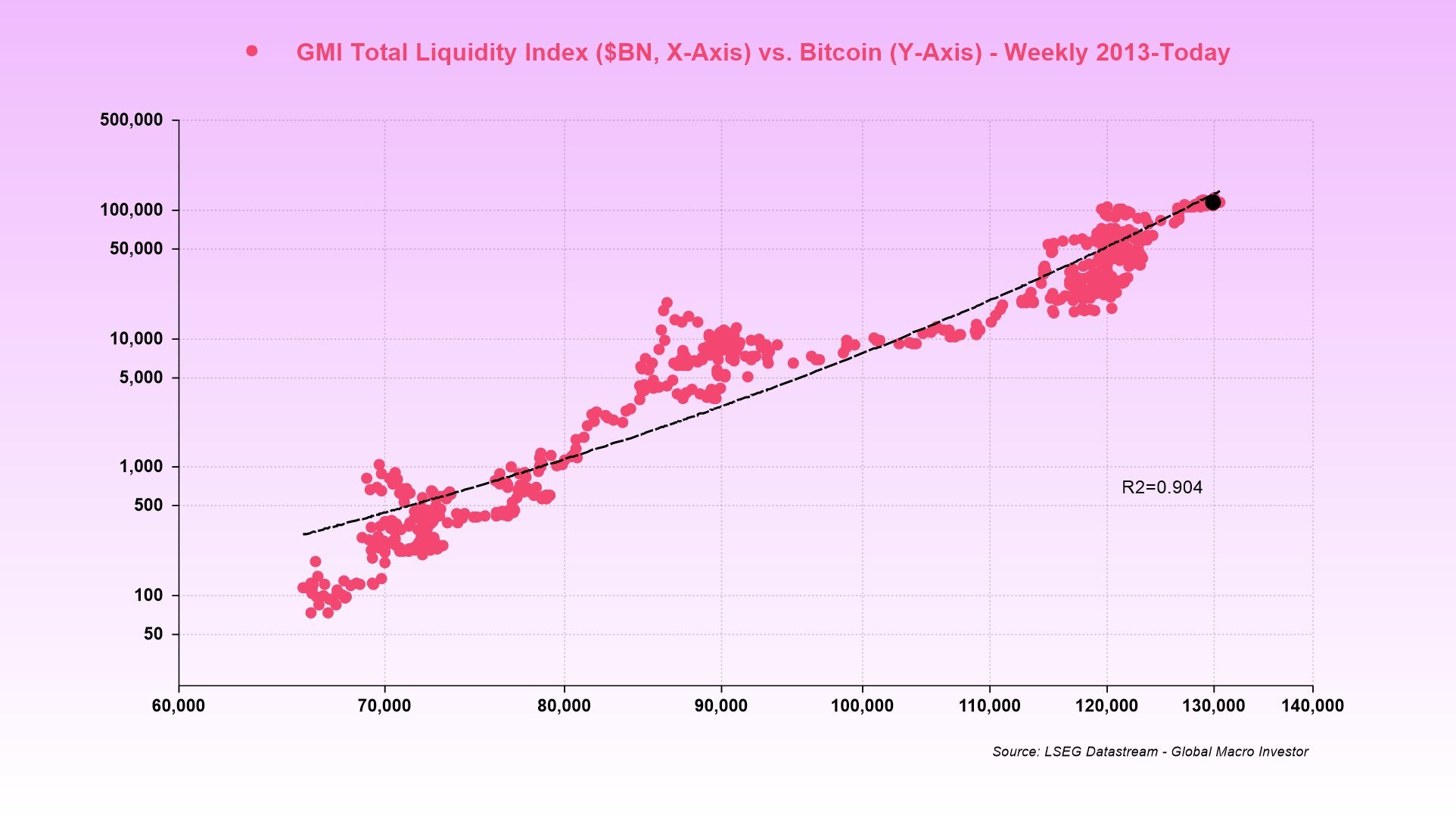

As outlined in the chart below, bitcoin’s price has remained largely in line with changes in global liquidity, suggesting that perhaps as global liquidity peaks, so will bitcoin’s price. However, market dynamics and bitcoin’s price as of March 2026 indicate that there will potentially need to be further downside for bitcoin and other risk assets before liquidity rises again. This scenario would mean the four-year cycle is intact as many assets would have seen sizable declines before sustained upward momentum returns.

While the additional liquidity provided through QE helps the government and corporations remain solvent, it devalues a currency’s purchasing power. Citizens can no longer accumulate cash savings or allocate capital to “safe” assets to plan for their retirement as interest rates on savings and more conservative assets end up with a negative growth rate. Instead, an increasing amount of capital needs to be allocated to riskier assets that have a better chance of outgrowing the rate at which the currency is debased.

For example, if inflation is 3%, while currency debasement is around 8%, then a person’s investments need to return at least 11% per year to maintain purchasing power. The S&P 500’s average return over a ten-year period is 10.5%. As companies, governments and individuals look for higher returns on their money, capital flows into riskier assets, such as crypto. This flow of capital aligns with the theory that bitcoin’s cycle will now extend as it matures. Its price will appreciate as global liquidity climbs, but it won’t experience the violent swings characteristic of previous retail-only cycles.

Is bitcoin’s four-year cycle over? It’s unclear.

The cryptocurrency market has been trading for just sixteen years—a relatively short time in the context of global financial markets. While the length of bull and bear markets has remained similar throughout previous bitcoin cycles, the entrance of institutional capital, macroeconomic correlation, and the reduced supply shock that comes with each bitcoin halving points to possible changes in bitcoin’s market structure.

It’s too soon to declare whether the cycle timelines are altered forever, especially given the last ATH was relatively recent, but the current market structure, count between the ATH and recent declines, and tight liquidity conditions indicate that the four-year cycle may likely still be intact.

Keeping current market dynamics in mind when you are considering your crypto holdings is critical at any time in the market cycle. Plus, with a long time horizon, holding bitcoin for long-term returns and as a store of value can be more effective than aiming to pick the top or bottom with absolute precision (something even seasoned market experts rarely get right).

Start building your crypto portfolio with Caleb & Brown

You don’t have to be an expert on bitcoin's market cycle to trade the original and largest cryptocurrency.

Caleb & Brown is the world's leading crypto brokerage for beginner and advanced investors alike, with bitcoin and hundreds of other crypto assets readily available for your portfolio.

Our personalised broker service makes crypto investing simple. A dedicated member of our broker team is always on hand to guide you along the way, giving you the confidence you need to navigate the world of crypto. Not to mention key features such as:

- One flat, transparent fee

- 300+ crypto assets available to buy, sell, and swap

- 24/7 customer support

If you're ready to take the next step and invest, contact your crypto broker today.

Not yet a client? Sign up for your free consultation.

from Caleb & Brown Cryptocurrency Brokerage.

.webp?u=https%3A%2F%2Fimages.ctfassets.net%2F4ua9vnmkuhzj%2FuIaUbUNRbO1LdljRWKvoI%2Fd93965ff275cd47f8c19fcc71edcd42e%2FBitcoins_Market_Cycle_V3-01__1_.jpg&a=w%3D3840%26h%3D2160%26fm%3Dwebp%26q%3D80&cd=2023-02-21T06%3A17%3A39.793Z)

.webp?u=https%3A%2F%2Fimages.ctfassets.net%2F4ua9vnmkuhzj%2F7meVnT2vnQelBrt6W5yw73%2F8469fbdea8168e404fff363b35dd65a4%2FBitcoin_Halving-01__1_.jpg&a=w%3D3840%26h%3D2160%26fm%3Dwebp%26q%3D80&cd=2023-01-10T02%3A22%3A06.649Z)